As noted in our January 3rd, 2024 notice to clients, on January 1, 2024, the Corporate Transparency Act (“CTA”) entered into force. The CTA requires “Reporting Companies” to report personal identifying information to the Financial Crimes Enforcement Network (FinCEN) about the individuals, within those companies, who are “Beneficial Owners” and “Company Applicants”. Such information will be maintained by FinCEN on a secure, non-public database for use by governmental authorities and financial regulators.

Who needs to report? The term “Reporting Company” is broadly defined to include:

Domestic Reporting Companies – any corporation, limited liability company, limited partnership or other business entity created by filing a document with the secretary of state or similar office in any state or territory in the U.S; and

Foreign Reporting Companies – any corporation, limited liability company, limited partnership or other business entity formed under the laws of a foreign country that has registered to do business in the U.S.

Who is exempt from reporting? There are 23 exemptions from the reporting requirement. Companies that quality under any of these exemptions will not need to file a beneficial report (unless they later become non-exempt). There is no requirement for potential Reporting Companies which qualify for an exemption to inform FinCEN that they are exempt. Some of the more prevalent exemptions include:

(A) ‘Large Operating Companies’ – entities that (a) employ more than 20 employees in the U.S. (no aggregation across subsidiaries is allowed), (b) filed U.S. tax returns during the previous year demonstrating over $5 million in gross US sales or receipts (revenues may be aggregated across subsidiaries) and (c) have operating presence at physical offices in the U.S.;

(B) wholly-owned or controlled subsidiaries of Large Operating Companies;

(C) publicly traded companies;

(D) companies operating in a regulated industry (e.g., insurance companies, banks, accounting firms, securities brokers dealers, securities exchanges or clearing agencies, public utilities, inactive entities),

(E) US-resident investment vehicles operated by investment advisors (i.e., private equity and venture capital fund); and

(F) non-profit entities.

What information must be reported? Reporting Companies will be required to disclose: (1) their full legal name, business address, jurisdiction of formation, and TIN, and (2) the identities of their “Beneficial Owners” and for each such person – his/her full name, date of birth, address and government-issued identification number). For Reporting Companies formed or registered after January 1, 2024, Reporting Companies will also need to disclose information regarding at least one and at most two “Company Applicants”, who are the individuals that (a) directly filed the document that created a domestic reporting company or the first to register a foreign reporting company and (b) who were primarily responsible for directly or controlling the filing or creation or first registration document (i.e., the company’s attorney and registered agent).

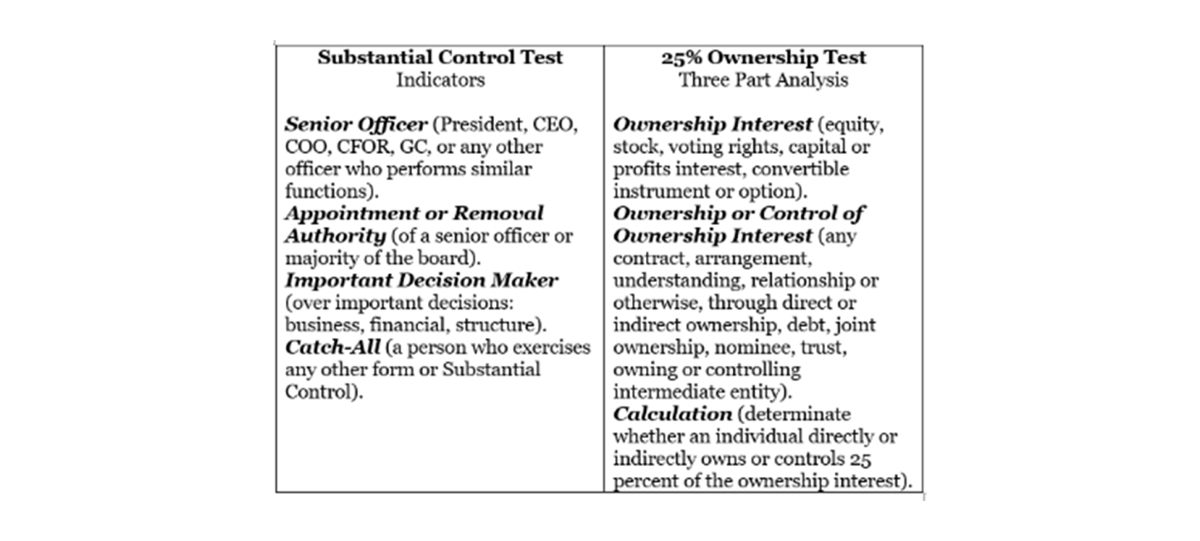

Who is a Beneficial Owner? “Beneficial Owner” is an individual who, directly or indirectly, owns or controls at least 25% of the ownership interests of a Reporting Company or a reporting trust, or who exerts substantial control over the company or trust.

Exceptions from Beneficial Owner definition, include: minor child, employee (other than senior officer), inheritor, creditor or custodian or agent.

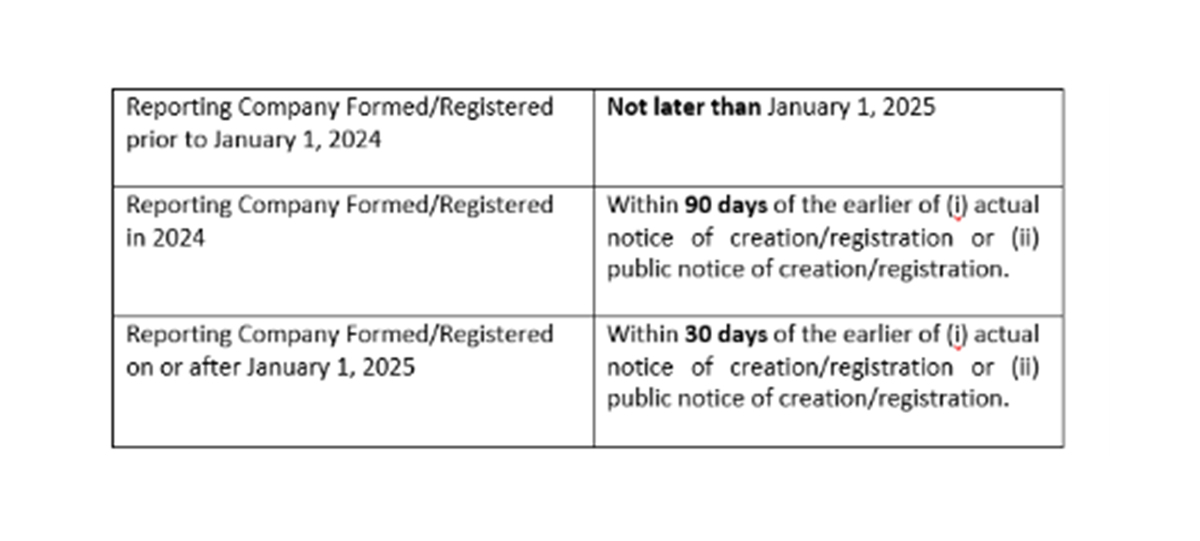

What are the due dates?

When are updated/corrected reports due? There is no annual reporting requirement. Updated reports are due within 30 calendar days after a change of previously information for Reporting Company or Beneficial Owner occurs. Corrected reports are due within 30 calendar days after a Reporting Company became aware or has reason to know of any inaccuracy. Data about Reporting Company’s Applicant does not need to be updated, assuming it was accurate when filed.

Where to send the reports? Reports are to be filed electronically using FinCEN’s secure filing system.

Are there penalties for non-compliance? Yes. Reporting Companies subject to the CTA could face civil and criminal penalties for willful failure to (a) report if required, (2) update Beneficial Ownership Information if required, and (3) correct inaccurate Beneficial Ownership Information. Civil Penalties can be up to $500 per day for every day of non-compliance (no maximum amount) and criminal penalties include a fine of up to $10,000 and imprisonment for up to two years. There is a safe harbor from liability and prosecution if the person who violated the CTA files a voluntary correction within 90 days.

What do you need to do to prepare for reporting? A. Determine whether a CTA exemption may apply. Companies within a large corporate structure will report on an entity-by-entity basis and need to be analyzed.

B. If an exemption is unavailable, it is imperative to take the following protective measures:

Identify Beneficial Owners & Company Applicants

Collect Information:Gather beneficial owner and company applicant information requiring disclosure to FinCEN.

Establish Protocols:Develop internal protocols to enable timely compliance with the CTA’s reporting requirements.

Review of Company Docs:Review entity governing documents and consider implementing revisions and updates to ensure CTA compliance.

Privacy Policy Updates:Review entity data privacy policies and consider revising same to better enable CTA compliance.

Educate & Train: Identify company applicants, and ensure each has sufficient knowledge and resources to properly comply with the CTA’s reporting requirements.

If you are wondering if you need to comply with the CTA, and if so, how and when, you should use our Interactive “Beneficial Ownership-Filing Test” in English and Hebrew below.

For any questions or further assistance in understanding your obligations under the CTA’s requirements, please contact James Raanan JamesR@apm.law or Dr. Tal Tirosh at talt@apm.law to discuss how these rules apply to your company.

This document is intended to provide only a general background regarding this matter. This document should not be regarded as setting out binding legal advice but rather as a practical overview that is based on our understanding. APM & Co. is not licensed to practice law outside of Israel.